NZ Business Survey and China Trade Data Set Asia Agenda Tuesday

Two policy-significant releases hit Tuesday's Asia calendar: New Zealand's QSBO and China's June trade figures ahead of Wednesday's GDP.

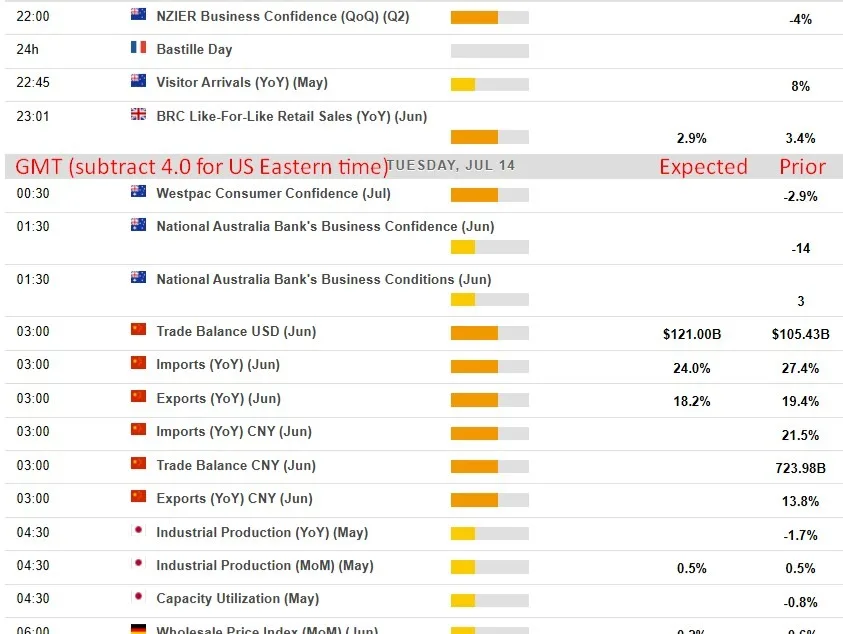

Two closely watched data releases are set to shape Asia-Pacific market sentiment Tuesday, July 14, 2026, as New Zealand's quarterly business survey and China's June trade figures arrive within hours of each other — each carrying implications that stretch well beyond their headlines.

The NZIER Quarterly Survey of Business Opinion drops at 2200 GMT, but analysts at Westpac and ASB warn the blended headline figure may obscure more than it reveals. Because the Q2 survey window straddled the mid-June Iran ceasefire, a split between early and late responses could give the Reserve Bank of New Zealand a clearer read on underlying sentiment than any single average. The critical question for the RBNZ is whether pricing intentions stayed elevated even after oil prices retreated from conflict highs — a sign that inflation pressure could outlast the geopolitical shock that helped trigger it. ASB is separately tracking capacity indicators after Q1 data showed labor constraints tightening for a second consecutive quarter alongside firms raising selling price expectations.

Read more US June Budget Deficit Hits $120B, Below Forecasts but Still Ugly →

China's June trade data is expected around 0300 GMT, arriving as a lead indicator one day ahead of the country's GDP release. Exports are forecast to ease slightly to 18.2 percent year-on-year from 19.4 percent in May, while imports are projected to slow to 24 percent from 27.4 percent. South Korean export data has suggested that Chinese import demand is concentrated in semiconductors rather than reflecting a broad domestic consumption rebound — a pattern that would reinforce the view that external demand, not homegrown spending, remains the primary engine of growth.

Forecasts for China's trade surplus vary sharply, from roughly 12 percent growth penciled in by cautious domestic research houses to near 20 percent expected by some international banks, with the surplus itself seen widening to approximately $120.6 billion. That divergence means the actual print carries outsized potential to reprice Wednesday's GDP expectations in either direction, making Tuesday's release a genuine market event despite its secondary billing.

Continue reading at Forexlive.